Why Savings Rate Matters Most If You Want To Retire Early?

Putting money away for your future often feels like deprivation. Most of us want to enjoy our hard-earned money right this second. Why shouldn't you? You've

For a few years in my early 30s, my savings rate was above 80%. I know that sounds extreme. It was extreme. But at the time it did not feel like deprivation. It felt like freedom arriving ahead of schedule.

I had gone from earning £20,000 a year as an employee to generating six figures through my own business within two years. The business was doing well, but because I was new to entrepreneurship, I was terrified of spending any of it. So I paid down my mortgage aggressively and put everything else into investments. My costs barely changed from my £20k days. That gap between earning and spending is what got me to early retirement at 40.

Your savings rate is the single most powerful number in your financial life. Not your salary. Not your investment returns. Your savings rate.

Most people get this backwards. They assume high earners have it sorted. They do not. I have worked with nearly 100 financial coaching clients, and I could count on one hand how many were saving 50% of their income. The majority were not even close. When I asked my Instagram followers if they could live on half their income, the response was almost unanimous: no.

So I asked a follow-up: If your life depended on it, could you live on 50%?

The answers flipped. Most said yes. Which tells you something. For the majority, not saving comes down to choice, not necessity.

Why I keep banging on about 50%

My audience is primarily in their late 30s and early 40s. Some have a solid foundation with money set aside for the future. Many are starting from zero. But nobody I speak to says they do not care about their financial future. The problem is that most are not putting enough away, by a long margin.

I use 50% because it sounds aggressive. It is aggressive. But when you look at the maths, a lot of people need to be aiming in that direction if they want to retire before they are forced to.

Retirement comes with the biggest pay cut of your life. Only you can counter that. And the tool you have is your savings rate.

Meet Sam and Pam

Sam earns £200,000 a year. Big car, flashy holidays, dinners out every week. He saves 20%. To the outside world, Sam is winning.

Pam earns £50,000. She is also doing well at that income, but she saves and invests 40% each year.

Who retires first?

Pam. By 15 years.

The maths behind it

Both Sam and Pam invest their savings and receive a 5% annual return after inflation. Both plan to use the 4% withdrawal rule in retirement (withdrawing 4% of their portfolio each year to cover living costs).

At a 20% savings rate, Sam needs 37 years of work to replace his income in retirement. At 40% savings, Pam gets there in 22 years.

Sam earns four times what Pam does. It does not matter. His expenses have risen to match his income. Like most people, he has built the life he wants and it costs what it costs. I get that. But if you spend to your means now, you will not be able to in retirement.

If Sam wants to hit his early retirement goals, he needs to make changes while the choice is still his, not when he is 65 and the choice is made for him.

Starting age changes everything

Here is what the numbers look like depending on when you start, assuming you want to retire around 60 and you are beginning with nothing:

- Age 20: Save and invest around 15% of your income

- Age 30: You need about 28%

- Age 40: Around 45%

- Age 50: You will need roughly 65%

The earlier you start, the less painful it is. I wish I had started at 20. I did not. I started seriously in my late 20s and had to be aggressive to compensate. That is the trade-off.

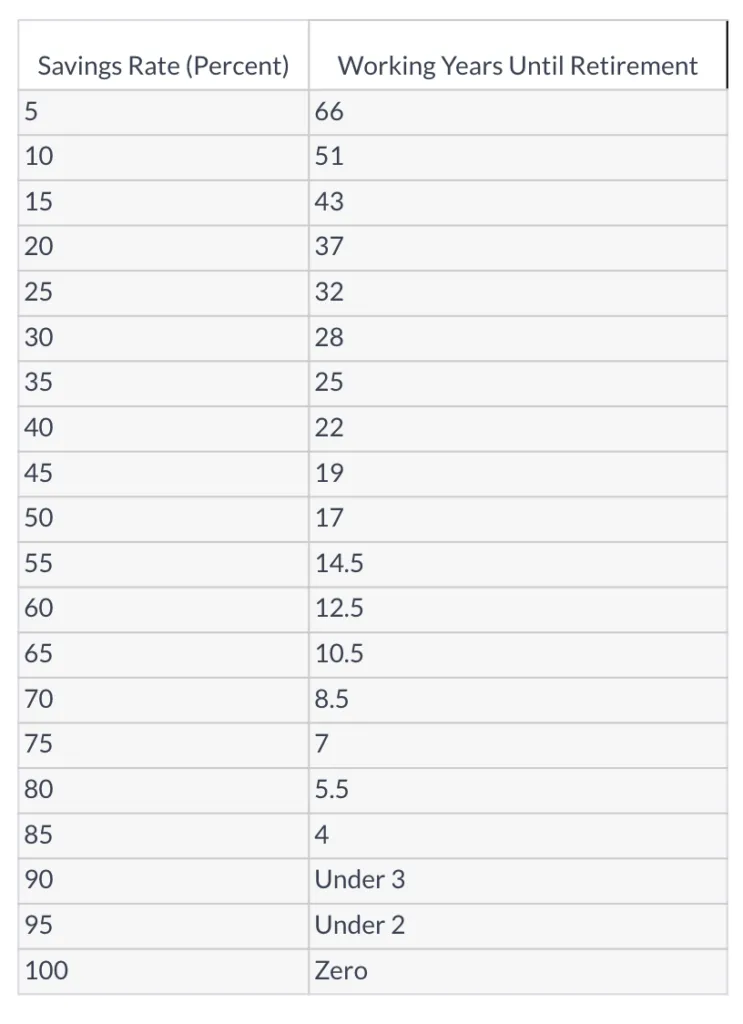

The article that changed my behaviour

This table was originally created by a blogger called Mr Money Mustache in his “Shockingly Simple Math Behind Early Retirement” article. If you have spoken to me about retirement for more than a few minutes, you will know I credit that article with changing the way I think about money.

His core argument is straightforward. How much you need to retire depends not on how much you earn, but on what percentage you save and invest. That reframing focused my goals on the three things I can control: earning more, spending less, and investing as much as possible.

It does not matter how much you earn. What matters is your savings rate.

How I got to early retirement in under 10 years

In some of those years, my savings rate was north of 80%. I had gone from a £20,000 salary to six figures, but I kept living the same life. I was not depriving myself. I simply had not inflated my costs, and the gap was enormous.

Few people would call an 80% savings rate anything other than extreme. But at the time, it was just maths. I was front-loading my investments while my income was high and my costs were low. That was the catalyst.

As the years went on, we did start spending more. Our savings rate dropped. Looking at the numbers, we averaged somewhere around 60-65% across the full journey. We did not track it obsessively, but I was always confident we were well above 50%.

You are probably looking at those numbers and thinking you could never save 80%. Fair enough. My challenge is this: can you increase your income while also reducing your spending? Even a little? You get to make that choice now, when it is your call. In retirement, when the income stops, the choice gets made for you.

Saving is not fun (at first)

I will be honest. If you have never focused on saving, the first few months are rough. You are saying no to things you used to say yes to. You are watching your mates spend freely while you are putting money into an index fund. It feels like you are missing out.

But the compound effect kicks in surprisingly fast. After a year, you have a cushion. After three years, you have momentum. After five years, you have options you never had before.

I have friends who respond to all of this with “What if I die young?” My answer is always the same: what if you do not?

Do not go to extremes

Some of you will read this and start penny-pinching every last pound. I would caution against that. Penny pinching now at the expense of living your life is no way to exist. I have said publicly that if I were starting again, I would maybe spend a little more and take a little longer on the journey. Planning for the future requires knowledge and balance. Knowledge to understand what you need to do, and balance to make sure you stick to the plan without making yourself miserable.

Enjoy the journey. Save aggressively, yes. But not at the cost of the memories and experiences that make life worth living.

Best of luck. And if you want more content like this, check out the Foundered Money YouTube Channel.

Keep reading

Written by Connor

Covering personal finance, investing, and the path to financial independence.

Enjoyed this? Get more like it.

No jargon, no spam. Just honest money tips, weekly.