How Much Do I Need To Retire? Bin The 4% Rule

How much do I need to retire is one of the most common searches for retirement. It’s a huge question and the short answer will always be “it depends”. There

How much do I need to retire is one of the most common searches for retirement. It’s a huge question and the short answer will always be “it depends”. There is no one-size-fits-all answer to this question as what works for you, will not be suitable for someone else. There are many factors within our own control and there are others on which we can exert no influence. The unpredictability of the future – the fluctuation of inflation rates, the stock market, the nature of support your family might require, or even the course of your own life – will make this a challenging task.

It can be easy to get overwhelmed due to the uncertainty you face. This uncertainty often results in fear, prompting many to remain in the workforce longer than they need to. When we are young, many of us focus on building wealth. Working hard and putting in long hours to climb the career ladder. In return, we hope to increase our income and put money away for our future. As you grow older, amassing wealth and resources, you eventually reach a stage where time and health are your most valuable assets.

You can buy a clock, but you cannot buy time

Matshona Dhliwayo

Many people continue to work and do so much longer than they need to. They save too much for their retirement. But then a life even happens. Illness strikes or the loss of a loved one reminds people of their own mortality. It is a stark reminder that the time we have is limited and we must live life to the fullest.

If retirement planning is so uncertain, then how can we have confidence in our retirement nest egg? How can we sleep at night when there are so many factors to consider? The answer is twofold: Knowledge and Adaptability. We must educate ourselves to understand what may influence our plans and be adaptable to change, because, it will inevitably happen.

In this article and video, we’re going to look at how much you need to retire. How you can retire with greater confidence through understanding some of the challenges and opportunities you might face and if you plan correctly, how you can retire even earlier. And with that welcome to Foundered Money!

The 4% rule

The 4% rule comes from a research paper by three professors of Trinity University (Not Dublin Trinity). This rule states that if you withdraw 4% of your portfolio every year, you can sustain your withdrawals for over 30 years. Many people who are focused on retirement, use the 4% rule as a guide to how much they might need. For every £100,000 saved and invested, they should be able to withdraw £4,000 per year, adjusted for inflation, during their retirement.

If you want to live off £20,000 in retirement, then you will need to save and invest £500,000.

£40,000 in retirement, a cool £1 million will be required to fund it.

Or if you want to do this based on your own figures, the quick and easy way to do so, is to take your current annual budget and multiply it by 25. If that figure scares you, then you might want to check out my other videos or article that will help you save money, increase your income and budget as efficiently as possible.

I’ll be the first to admit that I don’t necessarily agree with the principles of the 4% rule and I will be covering this in a future video. But there are many reasons why it is great. The top one is that it quantifies and simplifies the act of planning for retirement. It gives us something to aim for and for many this is a huge motivator.

However, to be completely honest saving £500,000 or £1,000,000 will be out of the reach of a lot of people. It will be impossible to do so. And when you mention big figures like this, they automatically switch off from the conversation. In fact, I have found, that some people negatively react to it, if they realise they won’t reach that goal. It’s a sobering reminder that our retirement may not be all we expect. So, if you’re in your 20s or 30s and watching this, put away 15% for your retirement starting right now. Thank me later.

In my opinion, the 4% rule doesn’t give us the full picture. The reality is, you can retire confidently with much less, provided you’re willing to be adaptable and ready to make necessary changes. Saving and investing more money is only one of the factors we need to consider.

Example of Trev & Bev

I’d like to introduce to you Trev and Bev.

Trev and Bev are a married couple in their late 40s and in retirement they aim to spend around £40,000 per year. Giving themselves another 10 years in the workforce, they are willing to focus on their retirement saving and make this a priority.

If we use the 4% rule, Trev and Bev would need £1,000,000 saved and invested at retirement age, to reach their target spending number.

Currently, their combined pension pots total £200,000 and they have no other savings. If we’re being completely honest here, this picture doesn’t look too promising for the couple. But maybe we’re not as wrong as you think.

There is still time

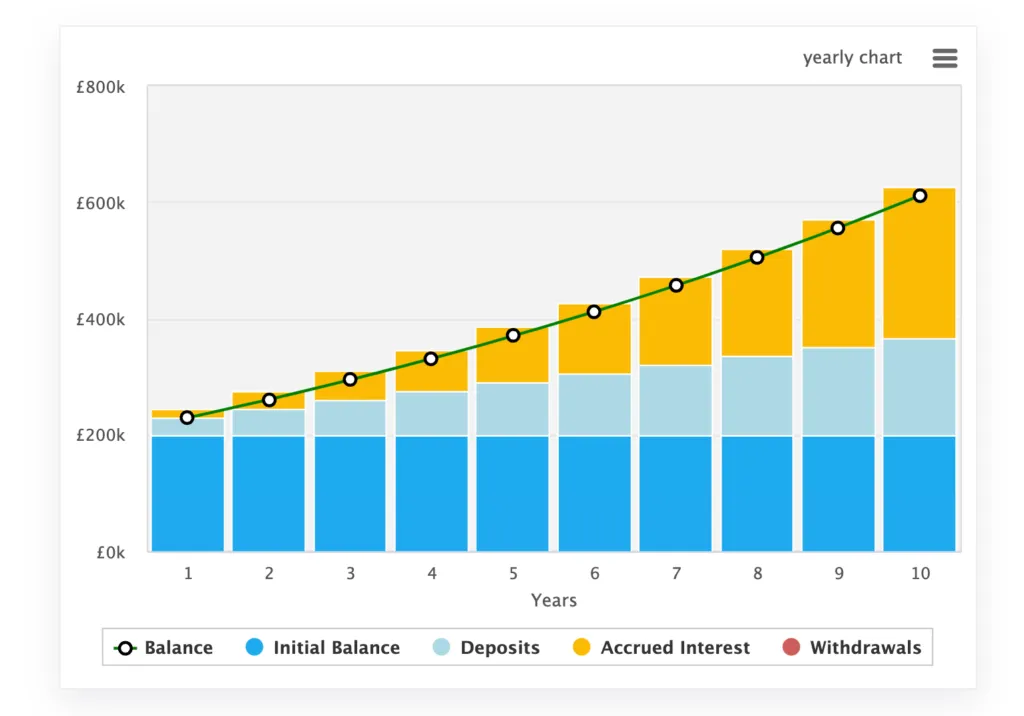

If we assume that Bev and Trev look at their situation and ramp up their pension contributions and are able to add £15,000 per year to their pensions and achieved 7% returns over the next 10 years. Their pension pots could then total £611,434.33. By continuing to keep paying into their pensions they’ll automatically get to 60% of their goal.

If they chose to take 4% of their workplace pensions following the Trinity Study, then around £24,500 at 4% of their total pension, could be taken. And for a lot of people, this will cover more than the necessities in their lives.

State pensions

And time isn’t the only benefit we have on our side. In the UK, the majority of us who have worked throughout our lifetimes will have accrued a full state pension. Which we must consider also.

For those of us around the age of 40 today, our State Pension Age is 68. Boohoo. Sadly the pension age is only going one way also. Up. However, at over £10,600 per year, per person, the State Pension does significantly reduce the amount we need to have invested. With a combined total of over £21,000 coming into the household in their late 60s from the state pension alone, the couple would be able to fully meet their financial goals, when they reach the state pension age.

However, as it stands Trev and Bev would have to significantly increase their withdrawal rate in the years between retirement and state pension age. This could have disastrous consequences for their finances and I would advise against it. However, once again, all is not lost. Trev and Bev have the opportunity and are willing to make changes now that will affect their retirement.

They could of course save more, but on the other hand, they could look at reducing their costs.

It’s also important to note that your private or workplace pension is normally available 10 years before the State Pension Age. If you want to retire before that age, which is 58 for anyone around 40 now, then you will need to find a way to fund this period before you can release your pension.And ISAs are a great way to do this.

Budgeting

Budgeting is the cornerstone of building and maintaining wealth. For most people who have not engaged in the ancient art of ruthless budgeting, there are always ways to trim the fat in a budget. Whether or not you want to is another matter. However, Trev and Bev could look at reducing their expenditure and leading a slightly less expensive life in their retirement. Sometimes retirement just costs less than working. 1 car rather than 2, eating out when at the office vs making homemade lunches. Living on less doesn’t mean a less exciting retirement. It may just mean that it’s time to stop paying for the diesel in your 30-year-old daughter’s car. Though I’m still livid at my mum and dad cutting me off on their Netflix account….

If you think about it like this – For every £1 Trev & Bev reduce their budget by, they would need £25 less saved/invested. Or for every £4,000 removed from their budget each year, £100,000 less is needed. It’s significant.

Downsizing your home

It might now be time to release some of the equity in your home through downsizing. It is not uncommon for many retirees being able to release hundreds of thousands of pounds in their property. Downsizing may not only release equity, but many retirees find themselves in “too much” home after their children have left. Empty houses still cost money to heat, light and insure.

Part-time work

Some early retirees choose to supplement their pensions with part-time work or consulting. By taking a lower-stress job or earning just a little bit each month through part-time work, you can significantly reduce the amount you need in retirement. Some use this money for the nicer things in retirement, others need this money as a necessity. Using 25x multiple based on the 4% rule, for every £4k you earn each year, you’ll need £100,000 less in your pensions.

I have spoken to countless retirees over the past year and many of them chose to work just a little bit longer to add additional money to their retirement. For some, this is a prudent move. You are currently likely in the highest-paying job of your career and looking for alternative income after leaving the workforce may mean you take a much lower rate of pay.

Last week I saw that McDonald’s is now actively recruiting retirees for their restaurant customer experience team. This may be a sign of the times, both in their ability to attract staff and the needs of retirees.

You have time to make the right decisions based on your needs. Be confident in your choices and move forward when you are ready.

Final thoughts

If we were to blindly follow the 4% rule then our only option is to keep saving more money until we reach the number that will afford our desired retirement income. However the 4% rule is not the only strategy we have and for many of us, our retirement plans will be a mixture of plans and ultimately our choices.

There is no right and wrong way, only what is right for you. And I hope this video has helped you to look at some of the other options available to you. Now, it’s over to you. Thank you once again for watching foundered money and building your knowledge and wealth with me. If you found my content useful or informative I would appreciate you subscribing to my channel or sharing my content with someone else.

If you liked the accompanying video or you think someone else might find it of benefit, I would greatly appreciate you sharing the Foundered Money Youtube Channel as far and wide as you possibly can.

Frequently Asked Questions

How much do I need to retire?

Following research conducted at Trinity University, you should aim to save/invest 25x your annual expenditure to be able to retire without running out of money.

Keep reading

Written by Connor

Covering personal finance, investing, and the path to financial independence.

Enjoyed this? Get more like it.

No jargon, no spam. Just honest money tips, weekly.