50/30/20 Rule: Budgeting Tips And Money

Budgeting is the cornerstone of personal finance. You will hear this from me time and time again. It's what will make you rich and keep you wealthy over the

Here’s a question: if I asked you right now where your money went last month, could you tell me? Not roughly. Precisely. Down to the pound.

Most people can’t. I couldn’t, for years. I earned decent money, paid my bills, went out at the weekend, and wondered why there was nothing left by the 28th. I wasn’t stupid with money. I just had no system.

The 50/30/20 rule changed that for me. Not because it’s revolutionary. Because it’s dead simple. And simple is what actually sticks.

What is the 50/30/20 rule?

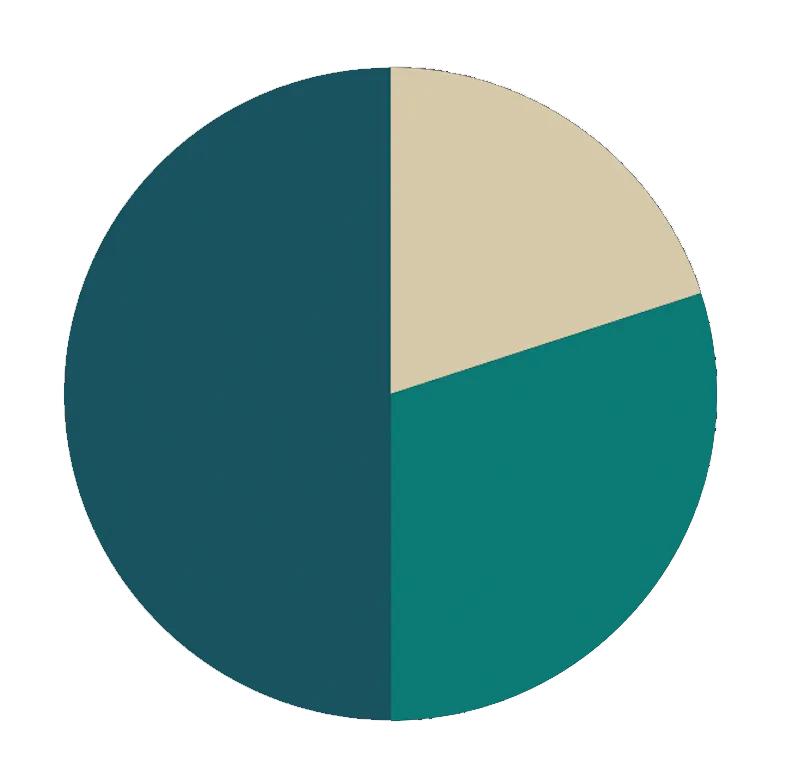

Split your after-tax income into three buckets:

- 50% on needs (essentials)

- 30% on wants (discretionary)

- 20% on savings or debt repayment

That’s the entire system. No complicated spreadsheets, no tracking every coffee. Three categories.

Start with your after-tax income

The 50/30/20 rule works from your total after-tax income. If you’re employed, that’s your net pay each month. If you’re self-employed and complete a self-assessment, use your profit minus expected tax payments. As a general rule, I suggest setting aside about 30% of profits for tax in the UK, though higher earners may need more.

So if your monthly take-home is £2,000, the split looks like this:

- £1,000 on needs

- £600 on wants

- £400 on savings or debt

These are targets, not commandments. Your situation might not allow this split immediately, and that’s fine. Working towards it is what matters.

Needs: the 50%

Up to half your budget goes on essentials. Rent or mortgage. Utility bills. Food. Basic clothing. Transport to work. Anything you genuinely cannot live without.

The key word is genuinely. Be ruthless here. Disney+ is not essential. Eating out is not essential. A holiday abroad, no matter how much you feel you need one, is not essential.

A useful test: if removing it would cause you physical harm or genuine danger, it’s a need. Your home? Essential. Heating in January? Essential. A Netflix subscription? That’s a want wearing a need’s clothing.

Wants: the 30%

Once your essentials are covered, 30% goes to the things you enjoy. Eating out, subscriptions, new clothes beyond the basics, hobbies, nights out. These are choices, not obligations.

We live in a world where advertising and social pressure push us to spend money on things we can’t afford. By capping this at 30% and being conscious of it, you stay within your means.

There’s overlap between needs and wants, and being honest about which is which is half the battle. You need food, but do you need to shop at M&S when Aldi does the job? You need clothes, but do you need designer brands?

I’m not here to tell you spending money is bad. Spend on what you value. Just be truthful with yourself about where the line is.

Savings: the 20%

This is the part that builds your future. Twenty per cent of your take-home pay, every month, put towards saving or paying down debt.

What you do with that 20% depends on where you are financially. Here’s how I’d prioritise it.

Build an emergency fund first

Have you got 3-6 months of essential living expenses saved and accessible? If not, start here. An emergency fund protects you from sudden financial shocks: a lost job, a car breakdown, a broken boiler. Without one, any of these could push you into debt.

Your emergency fund should cover 3-6 months of your essential costs only. In a genuine emergency, you’d cut discretionary spending entirely, so you only need to cover the necessities.

Using our £2,000 example: if your essentials are £1,000 a month, your emergency fund target is £3,000-£6,000. Keep it in an easy-access savings account. Separate from your current account. Untouched unless it’s a real emergency.

I’ll be honest, when I first built my emergency fund, it felt painfully slow. Putting £400 a month away while my mates were upgrading their cars was tough. But the first time I actually needed it (boiler died mid-January, naturally), I was glad I had it.

Pay down high-interest debt

Some people argue debt repayment should come before the emergency fund. I disagree. In a true emergency, being debt-free but cash-poor can leave you worse off than having savings and manageable debt.

That said, high-interest debt (credit cards especially) should be attacked aggressively. Always make your minimum payments, then throw any extra at the highest-interest balance first. The interest working against you on credit cards is the exact same compounding force that works for you when investing. Except it’s taking your money instead of growing it.

You can build an emergency fund and pay down debt simultaneously. The 50/30/20 rule is a guideline, not a rigid structure. Adjust the percentages to fit your situation. If you want to push your savings rate higher, shift money from wants to savings.

Invest what’s left

With your emergency fund built and high-interest debt cleared, the rest of your 20% should go towards your future goals. Saving and investing 20% of your income is substantial and will put you in a much stronger position than the vast majority of people.

The numbers add up faster than you’d expect. £400 a month is nearly £5,000 in a year.

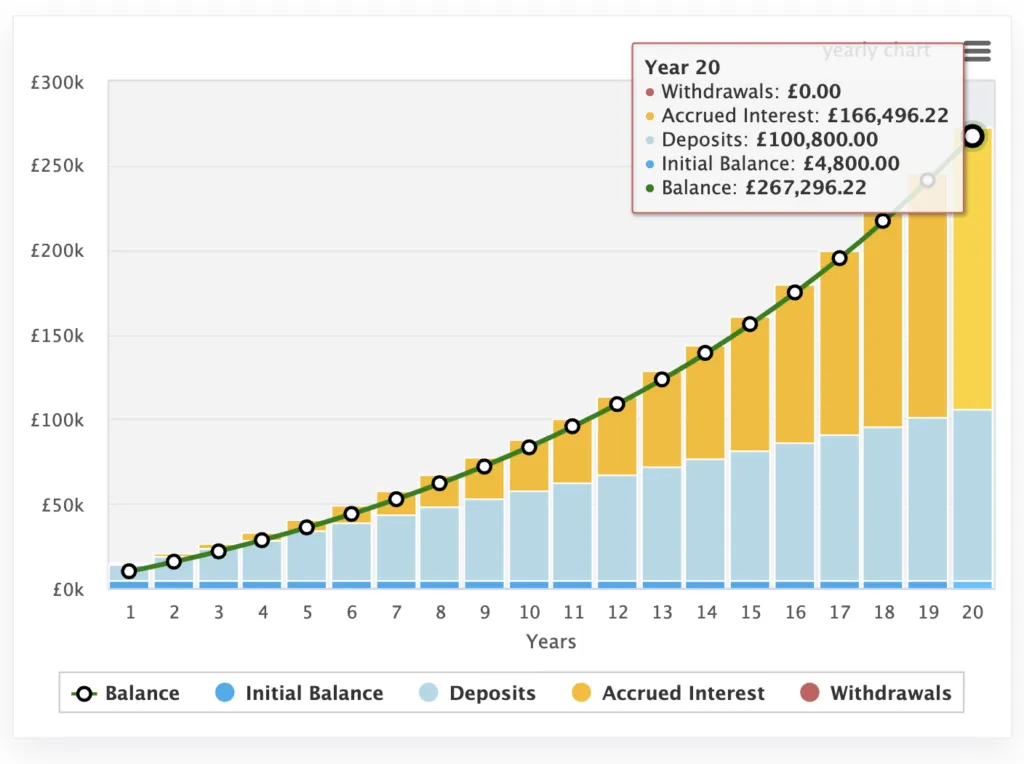

The power of compound interest

If you invest that £400 a month instead of just saving it, the results over time are dramatic. At an 8.5% annual return, £400 per month becomes over £267,000 in 20 years. The same compounding that punishes you when you’re in debt rewards you when you’re investing.

The goal is to start as early as you can and contribute as much as you can. I didn’t start investing seriously until my late twenties, and those lost years are the one financial regret I carry. If I’d started at 20, even with smaller amounts, the compound growth would have done the heavy lifting.

Final thoughts

Wherever you are financially today, the message is the same: start. The 50/30/20 rule is a guideline, not gospel. You can adjust the percentages to suit your circumstances, especially if you want to aggressively pay down debt or save for early retirement.

But as a starting framework, it works. Fifty per cent on needs. Thirty on wants. Twenty towards your future.

It’s not exciting. It won’t go viral on social media. But it’ll make you wealthy if you stick with it.

Want more content like this? Check out Foundered Money on Youtube.

50/30/20 rule calculator

Take home income £:

Necessities: £

Discretionary spending: £

Savings: £

Calculate

Keep reading

Written by Connor

Covering personal finance, investing, and the path to financial independence.

Enjoyed this? Get more like it.

No jargon, no spam. Just honest money tips, weekly.